Forward by NEFE

Meghan Sellers, Grants and Research Projects manager, NEFE

In the spring of 2022, the National Endowment for Financial Education (NEFE) surveyed 1,050 U.S. adults who identify as members of the lesbian, gay, bisexual, transgender, and queer (LGBTQ+) community to examine their quality of financial life. The results were telling: 39% of respondents reported their quality of financial life was worse than expected, while only 14% said it was better.

At the time, NEFE President & CEO Billy Hensley, Ph.D., identified a critical gap in visibility. He stated that the community remains systemically understudied, which directly mirrors the way they have been excluded from traditional financial opportunities. “The financial education field still has significant work to do to gather sophisticated data... the fact that in 2022 we still do not have the representative national data is a problem,” Hensley said, asserting that only through a, “deeper understanding of how this population is being economically restrained,” could intermediaries and advocates truly support this community.

In line with a commitment to stewarding robust and inclusive data, NEFE awarded a research grant to Casey Totenhagen, Ph.D., Melissa Wilmarth, Ph.D., and Heather Love, Ph.D., at the University of Alabama for “Finances in Sexual and Gender Minority Couples: Toward Inclusion in Family Financial Capability” as part of its 2022 research funding cycle. Below, Totenhagen, the project lead, shares the findings from their research, emphasizing a need for further validation of financial well-being measures across different populations, expanded access to financial education and increased inclusion within the financial services sector.

Financial Well-Being Looks Different Across Couples. Our Tools and Systems Need to Catch Up

Casey Totenhagen, Ph.D., University of Alabama

While there are many ways to think about financial well-being, such as how much money people earn or how much savings they have, a central component also has to do with how people feel about their financial lives, such as how stressed they are about money and whether they feel financially secure. Researchers, practitioners, and policymakers and advocates have long worked to identify ways to help promote financial well-being in people. However, these efforts have been viewed through a relatively narrow lens that has excluded consideration of sexual and gender minority (SGM) couples. Given disparities in both finances and health for SGM people (e.g., Borgogna et al., 2019; Lick et al., 2013; Stacey et al., 2022), this is an important gap—we need to better understand how to promote financial well-being in these couples to work toward closing these disparities. Supported by funding from the National Endowment for Financial Education (NEFE), our research set out to address these gaps.

We collected data from nearly 500 respondents, including gender minority people (e.g., transgender or nonbinary) as well as cisgender (i.e., those whose gender identity corresponds with the sex they were assigned at birth) people in different-sex (i.e. heteronormative couples) and same-sex relationships. Our project seeks to provide a better understanding of financial well-being in various types of couples so that policymakers and practitioners can best understand how to support them. Specifically, we examined whether widely used financial well-being measures are appropriate for use with different types of couples, how SGM couples experience access to—and discrimination in—financial services, and how their experiences related to finances are associated with other aspects of well-being such as mental health.

Financial well-being is about more than dollars and cents. It reflects the degree to which people feel secure about managing money today and whether they believe their financial future is stable and attainable. Those perceptions matter: financial well-being is closely linked to mental health, relationship quality and overall life satisfaction (e.g., Falconier & Epstein, 2011). Below we share early findings from our research that will help financial educators, service providers and policymakers work toward closing disparities for SGM couples.

A First Step: Making Sure We're Measuring Financial Well-Being Fairly

Before we can improve financial well-being, we need to ensure we are measuring it accurately across populations.

While a variety of tools are available to assess how people feel about their financial well-being, including the Consumer Finance Protection Board (CFPB) Financial Well-Being Scale, another commonly used tool is a 10-question survey developed by Netemeyer and colleagues (2018) that captures two important dimensions of financial well-being: The amount of stress they feel about finances right now (current money management stress) and what they anticipate their financial security might be like in the future (expected future financial security). While the scale performs well in general U.S. samples, it had never been validated specifically with sexual and gender minority individuals.

We used tests such as confirmatory factor analysis and measurement equivalence to test whether this tool was equally accurate across groups, including people in heteronormative relationships, people in same-sex relationships, and transgender or nonbinary people in relationships. The good news—it did. The tool captured financial well-being in comparable ways across different types of couples and can be confidently used in both research and practice with SGM populations. This matters because valid measurement is the foundation for identifying disparities, evaluating programs and informing inclusive financial policy.

Why Many Couples—Especially SGM Couples—Avoid Financial Services

Understanding financial well-being also requires understanding a person’s access to financial services that can be helpful, such as financial education or working with a financial planner. Prior studies have found that SGM people are less likely to have or be working with a financial services professional than heteronormative people (Copeland & Greenwald, 2022). We asked participants—in their own words—what has prevented them from seeking financial education or working with financial service providers, and whether they had experienced bias or discrimination in those spaces (NEFE, 2022).

We found in our data that across all couples, common barriers included cost, uncertainty about benefits, and perceptions that they are capable of managing finances without support from a financial professional.

But these barriers were not evenly distributed.

Gender-minority participants, who also had the lowest incomes among all groups, were significantly more likely to report cost as a prohibitive barrier, reflecting broader income insecurity and economic marginalization.

Concerns about trust and transparency also emerged, particularly among participants of color. Some worried about hidden fees or being steered toward products that benefited providers more than clients. Participants also feared consequences related to discrimination. One participant shared, “I … know that sometimes my race is seen as a negative to some of the provider's [sic] so I would also hesitate for that reason even if I felt I needed to seek out those services.”

For sexual and gender minority participants, concerns often extended beyond cost. Several described worries that providers would not understand or respect their relationships. One participant noted, “As a lesbian Indian/American couple, my partner and I once experienced subtle bias from a financial service provider when we applied for a joint loan at a bank... the loan officer seemed hesitant and asked invasive questions about our relationship, making us feel uncomfortable and unwelcome.” Some couples responded by intentionally seeking providers who demonstrated support of LGBTQ+ people, such as those who had advertised in gay media spaces.

Together, these findings suggest that access to financial services is shaped not only by financial knowledge, but by affordability, trust and whether people anticipate they will feel seen and respected.

Financial Lessons Start Early—and Not Everyone Gets the Same Ones

We also examined financial socialization, such as how people learn about money growing up through parental modeling, discussion and hands-on experience. Research shows these early lessons can shape adult financial behaviors and well-being (LeBaron-Black et al., 2023).

Results from our data showed transgender and nonbinary participants said they learned less about money from their parents compared with participants who were not transgender, regardless of the type of relationship they were in. These early gaps matter. For cisgender participants, stronger financial socialization was consistently linked with better subjective financial well-being in adulthood. The more financial socialization they reported experiencing from their parents, the lower their financial stress was, and the higher they expected their future financial security would be. For gender minority individuals, however, those links were absent, suggesting that traditional models of financial socialization may not fully capture their experiences or needs.

These findings have important implications. Policies implementing required financial education in schools should also consider integrating resources for parents on ways to connect with their kids about money. Still, efforts to close financial disparities may need to extend beyond education and address disrupted or incomplete financial socialization—particularly given the results for gender minority individuals. For those who may not have received sufficient financial socialization from their parents growing up, community-based and affirming interventions in adulthood may be helpful in closing gaps.

Financial Stress Doesn’t Stop at the Wallet

Financial well-being—and the lack of it—does not exist in isolation. Those who have higher financial well-being often benefit when it comes to their personal and relational health, too. We also examined how financial stress was linked to mental health and relationship functioning across these couples.

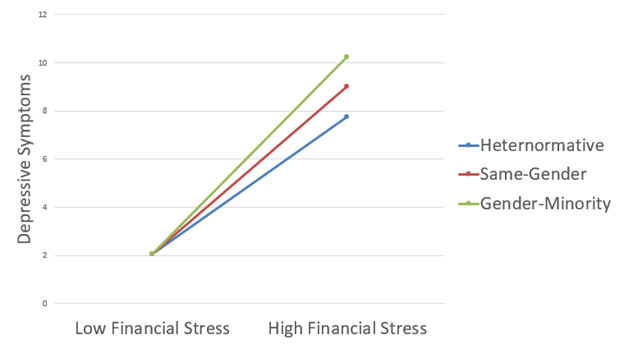

Consistent with other research (see Faconier & Epstein, 2011), higher financial stress was associated with more depressive symptoms and lower relationship quality for all groups of participants.

Importantly, however, the link between financial stress and depressive symptoms was strongest for gender minority participants. In other words, financial stress appeared to take a particularly heavy psychological toll for trans, queer, and nonbinary participants.

Graph demonstrating that while higher financial stress is associated with increased depressive symptoms for all groups, these effects were strongest for gender minority participants.

Together, these results underscore an important point: Reducing financial stress may have cascading benefits for all couples—and not just for financial outcomes, but for psychological health and relationship quality. Moreover, reducing financial stress among gender minority people may be particularly important, given they experienced the strongest effects of financial stress, as a path toward decreasing disparities in their psychological health.

What This Means for Research, Policy, and Practice

Our findings point to several takeaways:

- Researchers should continue validating financial measures across different populations. Although we found the measure we examined to be appropriate for use with different types of couples, other measures may have previously unexamined issues such as lack of inclusive language, or participants with different background and experiences may not interpret the items in the same way. Without inclusive tools, disparities may remain hidden or misunderstood.

- Policymakers should recognize that well-being—not just financial well-being but other aspects of well-being too—is shaped by both economic conditions and access to inclusive, affordable services. Policies that reduce discrimination and improve access can meaningfully support mental and relational health. Educators working with children should identify ways to extend resources to parents to encourage strong financial socialization—particularly children who may be gender non-conforming. Financial educators working with adults can work to better understand and consider the discrimination and bias SGM couples may experience in the workplace and when working with financial service providers and how these experiences can also shape financial well-being.

- Practitioners can make an immediate difference by prioritizing inclusive language, transparent fee structures, and explicit signals of affirmation for marginalized couples to help lower barriers and build trust.

Financial well-being is shaped by systems, relationships and early experiences. When we listen to SGM couples and design tools and services that reflect their needs and realities, we take meaningful steps toward greater equity for everyone.

References:

Borgogna, N. C., McDermott, R. C., Aita, S. L., & Kridel, M. M. (2019). Anxiety and depression across gender and sexual minorities: Implications for transgender, gender nonconforming, pansexual, demisexual, asexual, queer, and questioning individuals. Psychology of Sexual Orientation and Gender Diversity, 6(1), 54-63. https://doi.org/10.1037/sgd0000306

Copeland, C., & Greenwald, L. (2022). Retirement confidence survey and the LGBTQ Community. Employee Benefit Research Institute (EBRI) Research Brief. https://www.ebri.org/docs/default-source/pbriefs/ebri_ib_560_lgbtqrcs-14june22.pdf?sfvrsn=4a78382f_10

Falconier, M. K., & Epstein, N. B. (2011). Couples experiencing financial strain: What we know and what we can do. Family Relations, 60(3), 303-317. https://doi.org/10.1111/j.1741-3729.2011.00650.x

LeBaron‐Black, A. B., Curran, M. A., Hill, E. J., Toomey, R. B., Speirs, K. E., & Freeh, M. E. (2023). Talk is cheap: Parent financial socialization and emerging adult financial well‐being. Family Relations, 72(3), 1201-1219. https://doi.org/10.1111/fare.12751

Lick, D. J., Durso, L. E., & Johnson, K. L. (2013). Minority stress and physical health among sexual minorities. Perspectives on Psychological Science, 8(5), 521-548. https://doi.org/10.1177/1745691613497965

Netemeyer, R. G., Warmath, D., Fernandes, D., & Lynch, J. G., Jr. (2018). How am I doing? Perceived Financial well-being, its potential antecedents, and its relation to overall well-being. Journal of Consumer Research, 45(1), 68-89. https://doi.org/10.1093/jcr/ucx109

Stacey, L., Reczek, R., & Spiker, R. (2022). Toward a holistic demographic profile of sexual and gender minority well-being. Demography, 59(4), 1403-1430. https://doi.org/10.1215/00703370-10081664